The World Health Organization (WHO) stated that COVID-19 is no longer a global health emergency. Let’s take a look back at how the pandemic affected the aviation industry.

In March 2021, AviationSource released a book called “Aviation & COVID-19”, where we documented what the effect of the pandemic was on each individual segue of aviation.

The book particularly looked at the time period of March 2020-2021.

Over the course of today, each Chapter from the book will be released for our audience to read for free.

Without further ado, let’s get into it!

Aviation & COVID-19 Chapter 5: The Government Response…

One consistent theme that the COVID-19 pandemic has displayed, which has been seen in any industry, is the government’s response to the pandemic.

This chapter will look at examples of the UK, U.S., and European governments’ responses to the pandemic and whether more should or could be done to help the industry.

The United Kingdom

Across the industry in the United Kingdom, many of those have suggested that the government has not done enough to help the industry during these tough times. But have they done enough?

The subject of bailouts in the UK has been particularly controversial, especially with who it is going to and what the airlines have done with that.

This is something that will be compared to the United States’ approach to the pandemic.

The following two airlines have been bailed out by the United Kingdom Government (Transport & Environment, 2021)**:

- British Airways – €2,553,000,000 – Loan from HM Treasury and Bank of England’s coronavirus corporate finance facility at pre-crisis commercial interest rates (£300m/€343m). A further loan of £2bn (€2.21bn) was granted to IAG by the British government on the last day of 2020.

- easyJet – €2,240,000,000 – An initial government loan of GBP 600m (ca €670m) was provided at the start of the crisis, followed by a government-backed loan of GBP 1,4 bn (ca €1,570m) in January 2021.

With these two airlines came controversy because of the way they used the bailouts, which those in the UK were assuming would be used in the same way as the CARES Act in the United States was being used. To support jobs and not cut them.

Starting with British Airways, the airline itself was criticized back in May 2020 after turning “its back on a government bailout despite the fact that airlines across the world are being supported by their governments” (Spowart, 2020).

On top of this, the airline appeared to be at fault, especially with unions also arguing “that it is immoral and possibly illegal for the company to announce the swingeing cuts when it has received taxpayer money through the government’s coronavirus crisis schemes designed to protect jobs” (ibid).

Moreover, in that same month, the airline confirmed it was still going to press ahead with the 12,000-job cut, even with the government’s pledge at the time to extend the furlough scheme until October, which would have paid 80% of the wages within British Airways. Former IAG CEO Willie Walsh at the time said that despite the help that was offered, wage subsidy would not compensate for “the reality of a structurally changed airline industry in a severely weakened global economy” (Curry, 2020).

This could potentially offer the view that the UK Government had offered all it could to help the airline, but it seemed that Walsh had already made his mind up regarding the streamlining of the airline. However, the airline caved in eventually and acquired a bailout on New Year’s Eve 2020, managing to secure no conditions on the loan itself (Transport & Environment, 2021).

easyJet was another carrier to receive a substantial amount of money from the UK Government. With that, of course, came controversy not from the people but from the Founder, Sir Stelios Haji-Ioannou, who dubbed the bailout as “the biggest scandal in British corporate history” (AirportWatch, 2020).

He argued at the time that the bailout was used to pay part of a 107 aircraft order it has with Airbus, valued at £4.5bn (ibid). Haji-Ioannou even went to the extent of trying to remove the Chief Financial Officer Andrew Findlay to ensure the order does not go ahead properly.

This produced the view that the cancellation of the order would have provided easyJet with enough funds to survive beyond the original August deadline of running out of money completely (PA, 2021).

Such pressure eventually made CEO Johan Lundgren succumb to the words of Sir Stelios when in December 2020, the airline agreed to defer deliveries of aircraft from 2022- 2024 to 2027-28 (Ahlgren, 2020).

For a situation like this, it became understandable why the UK Government could have been criticized for handing this bailout to easyJet, especially if the funds were to be used for other reasons beyond the longevity and survival of the carrier during the pandemic.

As Sir Stelios mentioned, the deferral or, at best, the cancellation of the deal would have helped the airline majorly (PA, 2021):

“Terminating the Airbus contract is the only chance current shareholders have to maintain any value in their shares.

“If easyJet terminates the Airbus contract, then it does not need loans from the UK taxpayer and it has the best chance to survive and thrive in the future with some injection of additional equity provided for by the markets.”

“But if easyJet stumbles along whilst taking UK taxpayers’ money as loans only to pass it on to Airbus, it will have to raise fresh equity anyway in the next three to six months – reducing the value of our current shareholdings to close to zero.”

On those grounds, maybe the UK Government should have adopted more oversight when handing out the loans as they may have been able to have been acquired by other carriers in the United Kingdom who had been struggling substantially during the pandemic. The argument could have stretched as far as Flybe, but that, of course, was when the pandemic was just beginning and had issues of its own pertinent to BREXIT and huge losses at that time.

From the airline’s perspective, the UK Government may have to take some responsibility regarding the lack of oversight, particularly on the easyJet front when it comes to handing out taxpayer money to companies like that. In the eyes of British Airways, there was nothing that they could have done, irrespective of any bailout offers or furlough schemes. The airline was going to do it regardless.

Moving away from airlines and more into general policy, one thing that the UK Government was known for at the time was the 14-day isolation period for arrivals into the country. The Government believed that, at the time, it did the right thing (HoC Transport Committee 2020, p. 3):

“The Government justifiably acted on a precautionary basis when it introduced the time-limited self-isolation requirements for arrivals from all countries outside the common travel area.”

Whilst it has since been reduced to 10 days, those in the Government Committees believe that alternatives can be arranged instead of discouraging people to travel at this point.

This was evidently seen with the use of ‘air bridges’ being introduced to “enable people to travel between two countries with similar relative levels of infection without the need to quarantine” (HoC Transport Committee, 2020a).

Such air bridges were scrapped by the end of the Summer and into the Winter months when the second wave of the pandemic began to take hold of the country once again. With those in the committee arguing that the level of transmission rates are low in airports and on airplanes, it could have been suggested that the government’s lack of speedy action on the domestic front may have affected the recoveries needed within aviation.

With that in mind, of course, this is what resorted in airline associations calling for other forms of economic relief, such as Airlines UK’s call “for “a meaningful package of economic measures for airlines”, including a 12-month waiver on Air Passenger Duty, [which] steps to re-open travel markets through a UK testing regime for arrivals and more regional travel corridors” (Kennedy, 2020).

“Passenger numbers have collapsed, with most key aviation markets still subject to travel restrictions preventing airlines from generating revenues. Already, UK airlines have announced over 30,000 job losses, with 44,000 airline staff furloughed. The industry itself, and not just the UK’s status as the world’s third largest aviation market, is at risk.” – Airlines UK Spokeswoman – October 2020.

However, the recent UK budget of 2021 mentioned no help for aviation, especially with airlines and operators aiming to get passengers flying by the Summer, with Karen Dee, chief executive of the Airport Operators Association, calling this a major blow to the industry (Travel Weekly, 2021).

“Aviation has been the hardest-hit sector in the pandemic, but the Budget is blind to the impact of the near-complete shutdown of international travel”.

“While the extensions of the Job Retention Scheme and airport business rates relief are very welcome, they are not nearly enough given the scale of Covid-19’s impact. Combined with the long‑haul APD increase, which is a very damaging blow to an industry already on its knees, this is not a Budget for a global Britain.”

“The Scottish government and Northern Ireland Executive have already taken steps to continue crisis support for airports, including full-year rates relief in Scotland. The UK government must work urgently with devolved administrations to set out a four-nation Aviation Recovery Package of long-term financial and policy support to boost the recovery of the UK’s aviation connectivity.”

Of course, if you are looking at the health perspective of imposing strict rules such as quarantine for international arrivals, it may not have made a difference entirely, especially with the government being criticized for opening the economy too early.

This has been reflected even in a Times article published in March 2021, where the blame for the second wave damage was placed on the UK Chancellor Rishi Sunak due to his schemes of Eat Out to Help Out etc (Calvert & Arbuthnott, 2021).

Therefore, to bring such a sub-topic to a close, the reason why those in the industry are annoyed with the UK Government is because of its inability to impose the correct measures at the right time as well as not mentioning any help for aviation at all in the 2021 budget. And at the time of writing, as we begin to follow the roadmap to getting out of lockdown once again, there is always the chance of another wave hitting in the Summer.

The United States’ Response to Aviation & COVID-19…

As the pandemic began decimating the United States aviation industry, the Federal Government knew it had to do something, especially with domestic and international carriers feeling the pinch on a much larger scale than that of those in the United Kingdom.

So, the CARES Act (Coronavirus Aid, Relief, and Economic Security (CARES) Act) was passed, which has helped the industry in the U.S. considerably.

When it was signed into law back in March 2020, it incorporated support, valued at $10 billion, to airports alone, which in contrast to the UK Government, is exponentially more support (Federal Aviation Administration, 2020).

On top of this, Section 4112 of the bill authorized the Treasury Department “to provide up to $32 billion to compensate aviation industry workers and preserve jobs”, which was a massive lifeline that resulted in furloughs and job cuts to be prevented well into 2021 (U.S Department of the Treasury, 2020):

- Breakdown:

- Passenger Air Carriers: $25 billion.

- Cargo Air Carriers: $4 billion.

- Certain Contractors: $3 billion.

This program was recently extended back in March 2021 by an additional $14 billion, meaning that “the airlines will not be able to furlough, layoff, or reduce salaries for employees through September 30th, 2021” (Singh, 2021).

Of course, with each extension, a new area of uncertainty arises as a result, which may be posed to be similar to the thoughts of ex-IAG CEO Willie Walsh, where the cuts may need to be made either way. Matt Barton, Consultant at Flightpath Economics, believes that this is delaying the inevitable (Bushey, 2021).

“It seems like the system is a little bit on autopilot”.

“The industry is obviously still completely upside down. Does another extension simply delay the inevitable? Does it just make it harder for the industry to adjust?”

American Airlines has received the most amount of Payroll Support from the government, meaning that it has had to find other ways of funding, especially as the additional $14bn will not be heading all to American (ibid).

And this, of course, is the point that Barton was making, that the cuts may need to be made, especially with airlines having to raise debt because of them paying for everything else such as aircraft maintenance, parked aircraft, and much more.

The March 2021 extension of CARES is being seen more as an investment into the country’s infrastructure as opposed to propping companies up (Aratani, 2021).

“What this does is finish what we started – keeping the focus of the relief on the front lines”.

“This should get us through this pandemic to where the industry is building back to demand.” – Sara Nelson, international president of the Association of Flight Attendants-CWA

“By investing in the airline industry’s future, Congress is making a vital investment in our nation’s future.” – Eric Ferguson, president of the Allied Pilots Association

Another thing that the U.S Government is doing differently from the likes of the U.K Government is warranting shares in companies that take advantage of CARES as a form of oversight, with the Treasury expecting anywhere between eight and 20% shares in such firms.

It shows that if the funding is being spent in the wrong places, then the U.S Government can intervene a lot more freely, especially with the potential to own high percentages of the airlines and other companies to have a considerable say in such matters.

It is that high level of intervention that has been adopted by the new President Joe Biden, who is wanting to take more of a stronger involvement in the country’s overall recovery, with aviation being up there on the list of important industries.

However, there may need to be further government intervention when it comes to the safety aspect of the pandemic within the sector. Moran (2021) notes that American Airlines have issues that run deeper than the risk of bankruptcy, stating that its “focus is on cutting (most) costs to increase its profits – cutting ticket fares to gain market share, cutting safety measures faster than its competitors during the pandemic to put more passengers on flights, and so on.”

With the airline taking on more debt, this means that it will “have to spend more of the recovery period than its competitors simply making ends meet rather than trying to compete with other companies in the sector”, which puts the airline in more of a volatile position (ibid).

And such a volatile position it may be putting itself in may result in more jobs being cut on top of the 19,000 it has already cut during the pandemic, which is the most out of any U.S airline at the time of writing.

Of course, recovery is dependent on how the airline’s balance sheets are coping. Southwest for example, only had to make the decision to implement furloughs back in January 2021, which was the first cost-cutting measure regarding personnel, it had to make throughout the pandemic.

Whilst this sub-topic remains brief, it highlights that the United States, even when transitioning presidencies, remained highly committed to preserving jobs during this volatile time.

Of course, some jobs have been lost already because of this, but the Federal Government has done a lot to help minimize the number of losses within the industry.

It remains clear that the CARES Act may be prolonging the inevitable of the industry having to streamline post-COVID, which of course, will mean more job losses down the line. But in the presidency of Joe Biden, such a conversion of the CARES Act into a national investment program for the country, like that of Barack Obama’s Stimulus Plan, may prove to be beneficial for the industry along the way.

European Governments

European Governments have been taking a different approach when it comes to bailing out national carriers, using loan guarantees, state takeovers, and other options.

One major example of this is through German national carrier Lufthansa. According to Transport & Environment (2021), the airline has received a bailout of €6,840,000,000 but comes with the conditions of no dividend hand-outs and the German state owning a 20% stake in the carrier, with the option of increasing to 25% if a hostile takeover takes place.

The deal, which happened in May 2020, was the “biggest [bailout] by the German government in the wake of the coronavirus pandemic” (DW, 2020).

The European Union (EU) at first placed some resistance to this deal due to its approaches on State Aid discouraging competition, but with eagerness, the deal was able to go through in exchange “or Lufthansa making some slots available at its Frankfurt and Munich hubs” (Wilkes & Weiss, 2020).

For Chancellor Angela Merkel, this was deemed as quite a victory amongst the electorate as the country aimed to “revive the country’s export-led economy” (ibid).

It was also quite prominent for the rest of Europe, especially with the Lufthansa Group’s presence in countries such as Austria (Austrian Airlines), Switzerland (SWISS), Brussels (Brussels Airlines), and other countries due to subsidiary ownerships.

The EU would have agreed with the viewpoint that the State Aid would not have just benefitted German jobs but jobs across the rest of Europe due to Lufthansa’s enhanced route network pre-COVID.

The airline still needs to make around 500 million Euros in savings by 2023, so such cuts will still affect jobs down the line.

Another example would be the Air France-KLM Group (AF- KL), where bailout numbers are expected to exceed 14 billion EUR, with the French and Dutch governments propping up a lot of money to ensure the group remains afloat (Transport & Environment, 2021).

Such investments have been made for the same reason as Lufthansa due to the considerable European links it has across such member states. For a significant carrier like AF-KL or Lufthansa to hit, insolvency would mean the potential for the market to weaken and become volatile due to there being fewer links and routes.

Of course, there has been opposition to both groups acquiring state aid, as exemplified humorously by Ryanair Group Chief Executive Michael O’Leary, who referred to Lufthansa as a “Drunk Uncle at a Wedding” (Singh, 2020).

The Irish low-cost carrier also believes that such bailouts to Lufthansa, for example, will “further strengthen Lufthansa’s monopoly-like grip on the German air travel market” (Boon, 2020).

Because of this, it led Ryanair to target the German government by saying it “lectures all other EU countries about respecting EU rules” (ibid), hinting at the ironic political environment around France and Germany having considerable power within the European Union.

This, of course, has led Ryanair to instigate legal action against governments and airlines. Whilst it lost its case in February 2021, it will be launching appeals after continuing the accusative line of governments “selectively gifting billions of euros to their inefficient flag carriers” (Neate, 2021).

O’Leary, of course, has managed to maintain a strong position within Europe and is actively encouraging governments to open borders, even though insensitive ad campaigns such as the “Jab and Go” regime, which was later pulled as it was deemed “irresponsible” (BBC, 2021).

Even on O’Leary’s point of state aid being disadvantageous to airlines like Ryanair, British Airways, and others, governments are actively looking for cost efficiencies to be made in exchange for such bailouts being made.

For example, with Lufthansa having to relinquish slots at Frankfurt and Munich, that would open potential new routes for the likes of Ryanair, which is something that O’Leary should not particularly be bringing up as a problem, especially with Germany’s focus on exports, etc.

Either way, intervention within European Governments has been something quite strong, even despite such opposition by the likes of Ryanair.

As an opinion, it could be suggested that the obese and asthmatic structure of the European Union will, of course, help prop up obese and asthmatic airlines. It is the fact that the likes of Ryanair have streamlined its costs so much that it considers the legacy carriers as being in the way of being able to grow further than it had pre-COVID.

It remains clear that despite the structures, such legacy carriers need those bailouts; otherwise, the route network portfolios take a major hit and may not be as recoverable as others may think.

What do the people think?

Another indication of whether the government response is effective is through what the people think is sufficient, especially as they predominantly elect subsequent governments to bring their prospective countries forward during this pandemic.

Therefore, AviationSource conducted four studies, asking the following questions:

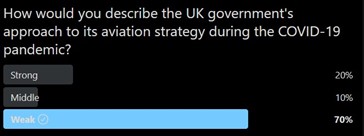

- How would you describe the UK government’s approach to its aviation strategy during the COVID-19 pandemic?

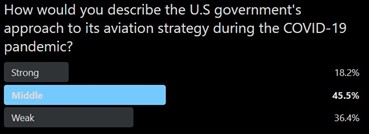

- How would you describe the U.S. government’s approach to its aviation strategy during the COVID-19 pandemic?

- How would you describe the European approach to COVID-19 aviation strategy?

- Do you believe that governments around the world need to invest more in the industry during this pandemic?

Questions 1-3 imposed a simple option choice of “Strong, Middle, or Weak”, with Question 4 posing as a simple yes/no question.

The first survey concluded with Weak taking the highest rating of 70%, stating that the UK Government has not done enough for the aviation industry to get it through this pandemic.

Most of this will be attributed to the government’s decision to impose hotel quarantine around a year after the pandemic started, as well as its inability to provide adequate funding to the industry, as stated in the United Kingdom sub-topic.

The second survey, which was based around the U.S. government’s approach to aviation during the pandemic, was more of a mixed bag, with 45.5% of entrants voting for Middle, indicating that it has been not good but not bad. 36.4% voted weak, which could be attributed to President Trump’s time in the Oval Office, as at the time of writing, President Biden’s additional support on the CARES Act had only been extended.

53.6% of entrants stated that the European approach to COVID-19 aviation strategy has been weak, with nearly 40% saying Middle.

The high support for Weak may have been attributed to Europe’s slow rollout of the vaccine, which in turn would hinder any potential roadmap for recovery going into the Summer of 2021 and beyond.

The final survey offered a resounding “Yes” when asked whether governments around the world should be investing more in the industry during this pandemic. With 76.2% voting yes, it highlights the need for further government intervention around the world by the respective administrations.

Overall

It remains clear that whilst some governments are intervening as much as they can in the aviation industry during this pandemic, more still needs to be done by governments, especially as we begin to see the light at the end of the tunnel.

However, as we have seen with some airlines who have made cost-cutting measures irrespective of bailouts or wage subsidy programs, British Airways could be onto something when it comes to prolonging the inevitable.

At some point, the financial support must stop, but at a point where the industry is more comfortable to do so. But with that in mind, those in aviation will be finding ways of bringing costs down, especially with recovery slated to be as far as 2024 at the earliest.

In the meantime, however, governments should be approaching the industry more and determining what needs to be done to ensure better short-term longevity and to keep the sector from collapsing.

stated that COVID-19 is no longer a global health emergency. Let's take a look back at how the pandemic affected the aviation industry.){kind=link}